From RSA with love – Retail Bonds

1. They offer better yields than conventional government bonds:

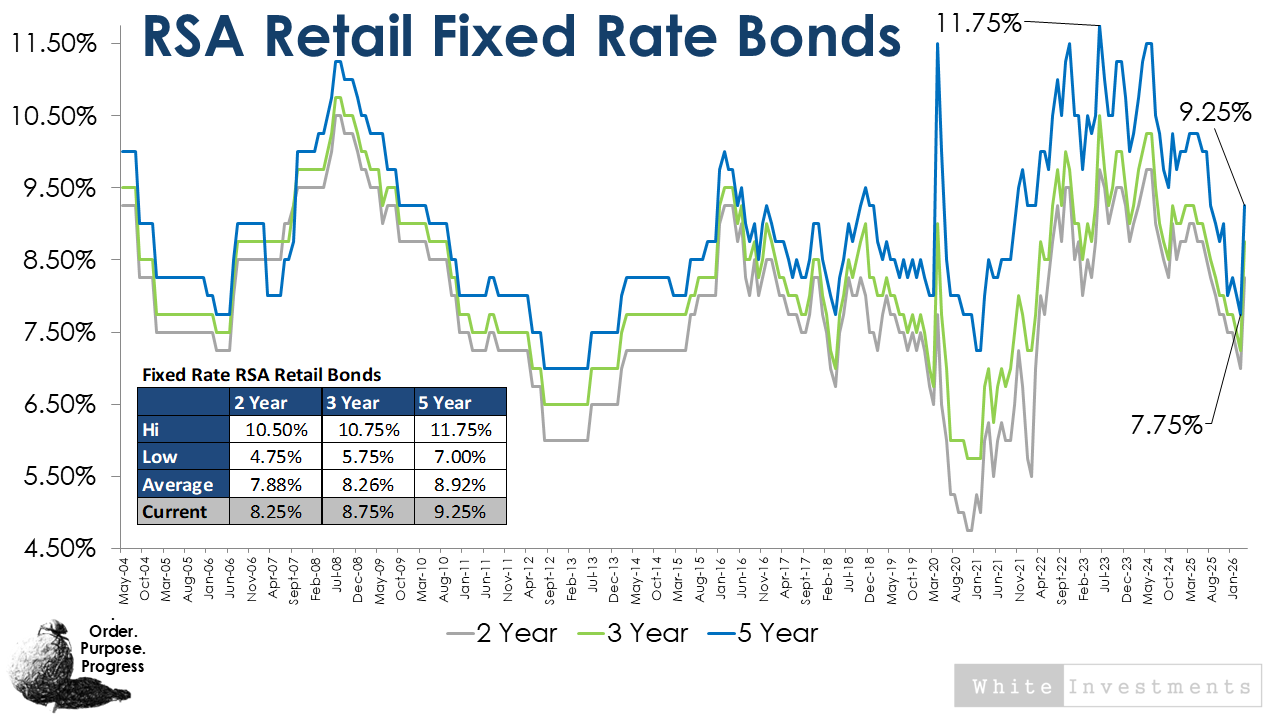

Most of the domestic bond funds you can invest in will have a majority allocation to South African government bonds (Govvies) of various maturities. The RSA retail bonds (RSA RB) pay a better rate than all of the similar dated conventional bonds and frequently better than most of the longer-dated equivalents too:

Without getting too technical, in “bond speak “ the longer you lend money for, the more you would expect to be paid – it is riskier to loan money over long periods and longer dated bonds have a greater sensitivity to changes in interest rates (duration). Retail bonds show there can be an exception to this rule, from time to time, so we should take advantage of that.

2. They offer better yields than the banks:

RSA Retail Bonds are issued by the South African government and not a bank or other financial institution. In most cases the banks would be expected to pay a higher yield or a premium to lend money from us relative to the government. But the SA Treasury is showing us retail savers a bit of love by offering a better return than most banks equivalent fixed deposit accounts.

3. They are low cost and easy to manage:

The RSA retail bond platform on which you purchase your bonds is absolutely free, gratis, mahala. It does not get cheaper than that and an investment can be set-up and monitored online. There are no hidden annual admin charges. There are no charges for reinvesting the income or making payments from your account. Unlike with the banks there are no requirements to hold other fee paying accounts, keep minimum balances or have minimum contributions. Whether you invest R1,000 or R5,000,000 you receive the same interest rate as everyone else.

4. The after tax yields are better than savings accounts pre-tax yields:

They are interest income producing assets which means you will be taxed at your marginal rate after you have utilised your annual interest income allowances (R23,800 for individuals under 65 and R34,500 for those older than 65).

But even at a higher marginal tax rate, the after-tax yield on the 5 year retail bond would probably beat the pre-tax yield of about 99% of instant access savings accounts at the bank.

That could be food for thought for those of you holding long-term cash positions in your bank accounts.

5. Liquidity:

This is often cited as the main drawback of the RSA Retail bonds. These bonds are not tradable on a secondary exchange which means once you have bought them you must hold them for the duration of the agreed term. After a year you may access your money but you will be penalised, by forfeiting any interest income still owed to you.

This is similar to the offerings from fixed term accounts at the bank. I have no problem with this as it promotes discipline and averts the cheeky dip into savings from time to time.

5. SA Treasury give you a free option:

One of the most unique characteristics of the RSA Retail Bond, and a very compelling one at this stage in the interest rate cycle, is the RESET OPTION. Basically the Treasury is saying invest in a bond at an agreed fixed rate. After 12 months if the rate is higher we will give you the option of switching to that higher rate by re-setting your investment. Most financial institutions would charge you a hefty fee for this option but our friends at the treasury illustrate the willingness to promote savings by giving it to you for free.

6. They can offer the best real yields (Inflation beating):

It is often said that the only sane definition of wealth is maintaining your purchasing power.

That means making sure that each Rand you save and invest can buy you the same or more each year.

For that to happen your money must grow faster than the cost of living increases.

It should be noted here that you can also invest in inflation-linked RSA retail bonds. Unfortunately there is too much to cover in detail in this write up but the choice to go fixed or inflation-linked depends on current pricing, your time horizon and your future inflation expectations.

0 comments