The South African government issues RSA Retail bonds.

While I have stolen the idea for the title of this article from an onscreen icon, I will not go into too much of a cheesy metaphor related to the suave British Secret Service Agent, 007.

Suffice to say that the similarities begin and end with the name – Bond.

So what are RSA Retail Bonds

In truth there is nothing sexy about RSA Retail Bonds. They are how you loan the South African government money in return for some, more often than not, very favourable interest payments.

Retail Bonds exhibit none of the “sex and violence” traits that make for a captivating bond movie storyline or sales pitch.

They offer none of the adrenalin pumping excitement often associated with stock-picking, where the promise of great riches creates a world of heroes (Apple Inc) and villain’s (African Bank).

It is their boring predictability that makes RSA retail bonds my investment of choice in many circumstances. There are many reasons why I think you could consider them too.

Why invest in RSA Retail bonds

1. Retail bonds offer better yields than conventional government bonds:

Most of the domestic bond funds you can invest in will have a majority allocation to South African government bonds of various maturities.

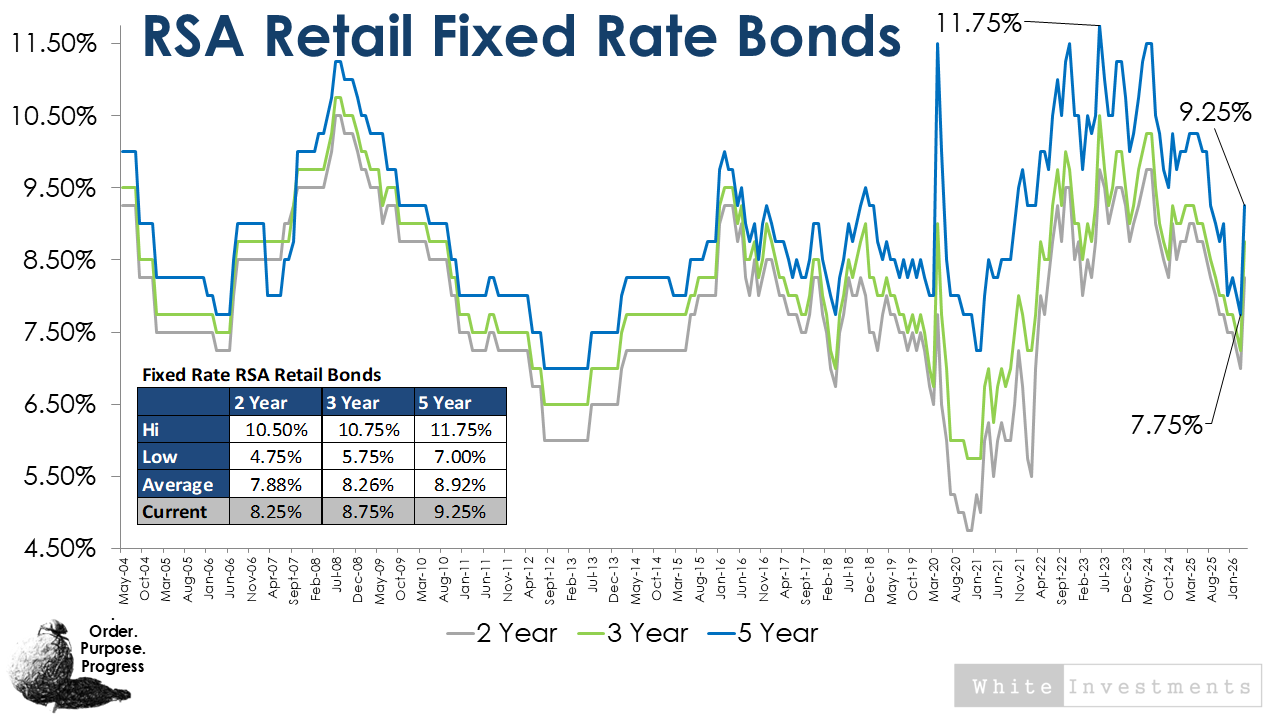

The RSA retail bonds (RSA RB) pay a better rate than all of the similar dated conventional bonds. Frequently better than some of the longer-dated equivalents too.

Without getting too technical, in “bond speak “ the longer you loan money for, the more you would expect to be paid for it. It is after all riskier to loan money over long periods.

Bonds with long maturities have a greater sensitivity to changes in interest rates too (called duration), so higher yields and shorter maturity dates are good value.

2. Retail bonds offer better yields than the banks:

RSA Retail Bonds are issued by the South African government and not a bank or other financial institution.

In most cases the banks would be expected to pay a higher yield, or a premium, to borrow money from you relative to the government. But the SA Treasury is showing retail savers a bit of love by offering a better return than most banks equivalent fixed deposit accounts.

3. They are low cost and easy to manage:

The RSA retail bond platform on which you purchase your bonds is absolutely free, gratis, mahala.

There are no hidden annual admin charges, no charges for reinvesting the income or making payments from your account.

Unlike with the banks there are no requirements to hold other fee paying accounts, keep minimum balances or have minimum contributions.

Whether you invest R1,000 or R5,000,000 you receive the same interest rate as everyone else.

You can apply online.

4. The after tax yields are better than savings accounts pre-tax yields:

Retail bonds are interest income producing assets which means you will be taxed at your marginal rate. Remember though, you have an annual interest income allowance.

R23,800 for individuals under 65 and R34,500 for those older than 65.

Even at a higher marginal tax rate, the after-tax yield on the 5-year fixed retail bond would probably beat the pre-tax yield of about 99% of instant access savings accounts at the bank.

That is food for thought for those of you holding long-term cash positions in your bank accounts. (Or alternatively, lets chat and get your money working smarter for you).

5. Liquidity:

This is often cited as the main drawback of the RSA Retail bonds. These bonds are not tradable on a secondary exchange which means once you have bought them you must hold them for the duration of the agreed term.

However, after a year you may access your money by making a special request, but you will be penalised, by forfeiting any interest income still owed to you.

6. SA Treasury give you a free option:

One of the most unique characteristics of the RSA Retail Bond, and a very compelling one when interest rates are low, is the RESET OPTION.

Basically the Treasury is saying, “Invest in a bond at an agreed fixed rate. After 12 months if the rate is higher we will give you the option of switching to that higher rate by re-setting your investment.”

Most financial institutions would charge you a hefty fee for this favourable option, but our friends at the treasury illustrate their willingness to promote savings by giving it to you for free.

7. Retail bonds can offer the best real yields (Inflation beating):

It is often said that the only sane definition of wealth is increasing your purchasing power.

That means making sure that each Rand you save and invest can buy you the same or more each year.

For that to happen, your money must grow faster than your cost of living increases.

It should be noted here that you can also invest in inflation-linked RSA retail bonds. Unfortunately, there is too much to cover in detail in this write up. The decision to go fixed or inflation-linked depends on current pricing, your time horizon and your future inflation expectations.

When should you consider using RSA retail bonds?

I am not advocating RSA retail bonds are the Holy Grail of investment options which will suit all circumstances.

They are NOT instruments for creating long-term wealth.

If you have a long-term time horizon and no need for income, then you should focus on equities, property or other growth related investments. Over the long-term, these should provide you with the best real returns.

Matching known future costs or liabilities.

However, if you have a defined goal with a 5-year or less time horizon you can potentially match your future liability with absolute certainty using RSA Retail Bonds.

Unlike with a share purchase, the beauty of a bond is that you know right upfront what cash flow (payments) you will receive and when you will be getting them.

If you are already in retirement and looking for regular known payments these may come in handy for short-term cashflow generation too.

What else do you need to know about RSA Retail Bonds?

These bonds are, as the name implies (retail), only available to individual South African residents.

So you cannot buy them in a trust, partnership, as a company, collective investment scheme or as a non-resident. (I believe it is mostly as a result of this restriction that the yields available on these bonds are still so attractive).

Sadly, they are not currently even available in a Tax Free Savings Account either but I know there are rumblings about changing this.

You can opt to get paid out your interest or you can have it reinvested and compounded over the life of the bond. HINT: Get it paid out for cashflow or income needs but compound it if you don’t need the income.

You can (and always should) nominate beneficiaries to avoid the executor fees for estate planning purposes. Note they will still be subject to estate duty.

RSA retail bonds are certainly not an investing panacea but they are often over looked relative to other more mainstream (and well marketed) options. If you would like to find out more about RSA Retail bonds you can visit their website or get hold of White Investments who can help you incorporate these instruments into a successful financial plan.